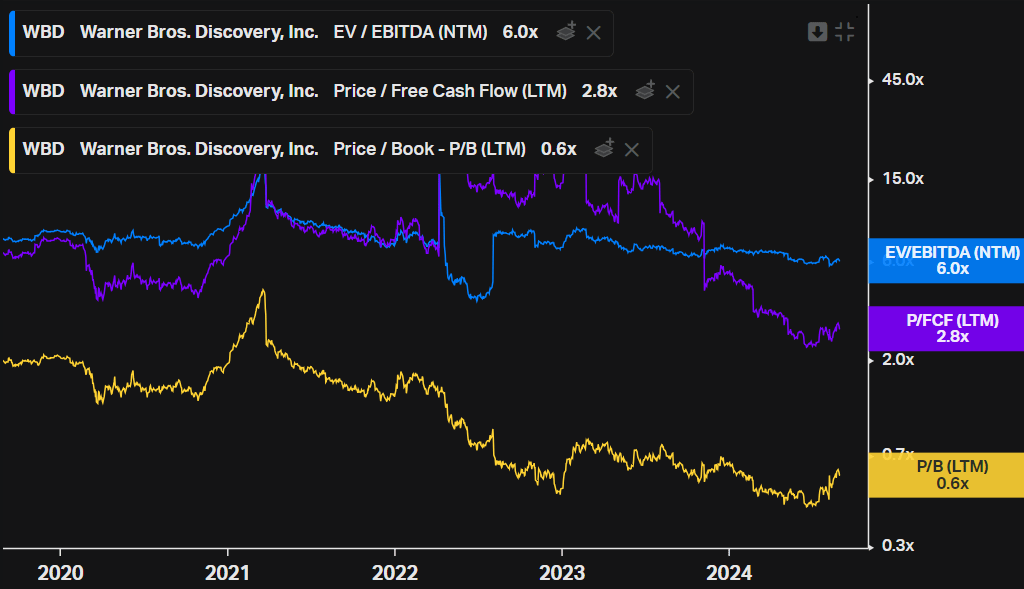

Warner Bros. Discovery (NASDAQ:WBD) stocks once again traded below $7 after weak Q2 earnings, and although it has already returned to a level close to $7.7, at this level, the company is one of the cheapest telecoms, trading at multiples of 2.8x price-to-FCF (LTM) and 6x EV-to-EBITDA over the next twelve months.

This high asymmetry in valuation and other positive factors in earnings, such as the addition of subscribers, were overshadowed by bigger problems. One of them was that the company booked -$9 billion in losses related to the value of its legacy TV operations (non-cash), which highlights the poor state of the industry and that these operations are worth less than the company previously expected. Not only that but there was also a miss in revenue and reported weak Studio and Networks data.

Even with Warner Stocks under pressure, it is necessary to be extra careful, as the company now becomes both a candidate for a value move and a value trap. In the last article, my rating for Warner Stocks was ‘buy’, based mainly on the strength of its IPs, a clearer turnaround (with even less bad earnings) and, of course, its asymmetric valuation. In view of the change in the current context (even if it’s not such a drastic change), a ‘hold’ rating seems more effective in the current period (and I’m keeping the shares I own).

Warner Stocks Remain Undervalued

In several metrics analyzed, Warner Stocks are undervalued. After the merger with Discovery, there was a strong compression of multiples as problems arose and financials did not come in as the market expected.

The combination of the businesses showed substantially higher revenue, but that has been declining in recent quarters, along with an EBIT that has also shrunk. It’s worth noting that analysts already expect a certain upturn in the coming years, with revenue only gradually advancing and EBIT returning more. As already mentioned, the multiples have come under a lot of pressure due to the falls in stock price, the free cash flow price is less than 3x, the EV-to-EBITDA forward is 6x, the price-to-book is 0.6x and, most interestingly, the free cash flow yield in relation to EV (i.e. taking into account the high debt) is 11.75%.

Koyfin

For the consensus, in the medium term, there is hope for stability/an upturn in financials. For 2025, the market expects a ~5% growth in EBITDA, reaching $9.64b and bringing EV-to-EBITDA to 5.9x. The market also expects positive EPS (non-GAAP) in the same period, around $0.43 per share, which would give us a price-to-earnings ratio of 18x.

If a recovery scenario were to materialize – with stable revenues and improved profitability – these multiples could be even lower and more attractive in the long run. Still, it’s worth reiterating that the operations carry a lot of risk. Both the Income Statement and cash flow indicators could continue to shrink in the short, medium, and long term, which is precisely why these multiples are so low (and why I’m downgrading the rating).

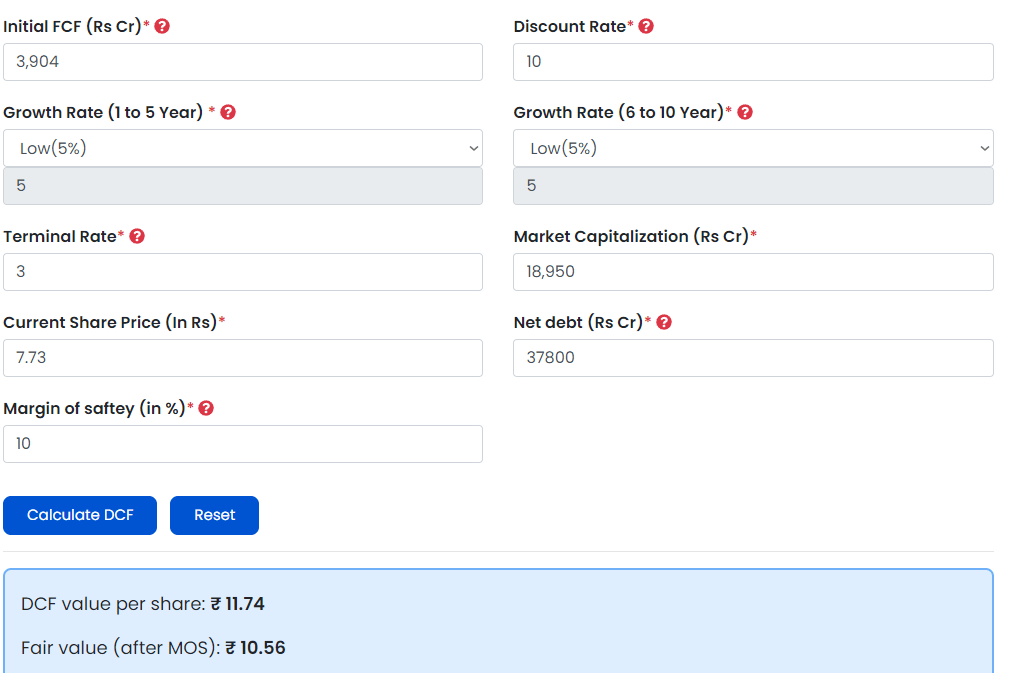

In Q2, the company posted a $1.2bn decrease in cash from operations and a $1bn decrease in free cash flow. Even so, this free cash flow was $976 million in just one quarter, since major factors that compress net income are non-cash, such as $7.7bn of content rights amortization in the last six months and depreciation of $3.6bn. Therefore, if we perpetuate a similar level of cash generation for the long term and bring it to present value, it is possible to find a good upside.

Annualizing the free cash flow of Q2 (which has already shown a good decrease), with growth of 5% per year for the next decade, with a terminal rate of 3%, after a margin of safety of 10% we would still have a fair value of ~$10.5 for Warner Stocks, which would be an upside of more than 30% just if Warner manages to get back on track and achieve reasonable growth.

Finology.in

The problem is that this growth is not so clear, and with the latest results, it is difficult to estimate when the company will return to sustainable growth at this level. Just by sticking to the assumptions and discounting by a higher rate such as 11%, you can already find a fair value closer to today’s stock price, around $7.4 after the 10% margin of safety.

Warner’s Q2 Struggles: Weak Earnings and Declining Revenues

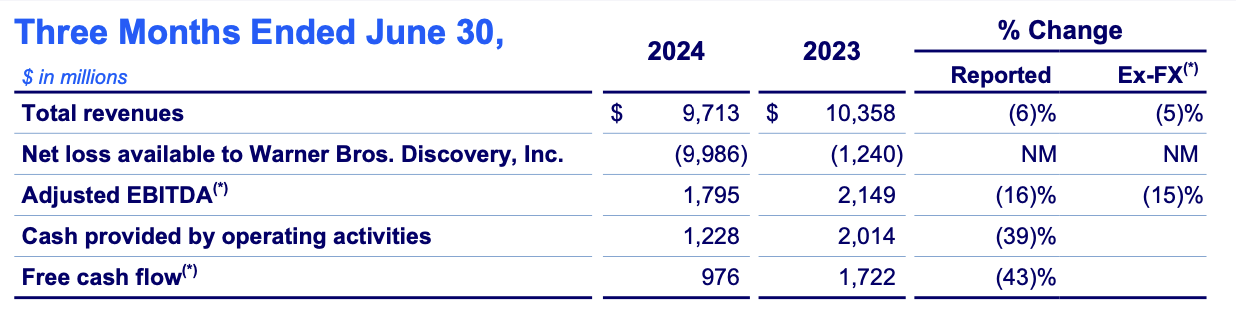

Just looking at the highlights of the quarter, you can see that it wasn’t good. The total revenues declined by 6%, adjusted EBITDA was even worse, down 16%, while free cash flow shrank by 43%. While the reported revenue was $9.7bn, the market expectation was $10.07bn, which would be a slightly smaller decline than the one presented, while the estimated EPS was -$0.22 while the reported one was -$0.36.

Warner Bros. Discovery’s Earnings Release

In the breakdown, Studios performed poorly. TV revenue declined 27% YoY; Games declined 41% due to the weak performance of Suicide Squad and a strong base of comparison with Hogwarts Legacy; the only silver lining was that theatrical revenue increased 19% with Dune: Part Two. With the higher SG&A and content expense costs in theatrical, EBITDA in this segment shrank by 31%.

Networks delivered something close to the expected trend, with the lower relevance of cable TV, networks, this type of advertising, and the like. But this decline is accelerating, with both revenue and EBITDA down 8% YoY.

In my opinion, DTC showed the best results, although they were also mixed. Revenues fell by 6% due to lower content revenues, which fell by 70% due to a lower volume of third-party licenses. On the other hand, advertising revenue increased by 98%, while distribution remained stable. Despite a slight drop in subscribers in North America, other regions sustained growth, bringing total DTC subscribers from 99.6 million in 1Q24 to 103.3 million in 2Q24, with global ARPU also increasing from $7.83 to $8.00 in the same period. As a good part of the strategy to sustain operations in the long term by monetizing DTC, an improvement in these operating indicators even with a drop in content spending is welcome and somewhat clears up the expectation that one day this segment could be profitable and partially offset the declines in Networks.

Another point that was highlighted by the media was the non-cash impairment charge of $9.1 billion, to make more sense of the value of the network operations after the faster-than-expected declines and also the loss of the NBA.

Combining all these factors, we have a net loss of -$10.9bn in the last six months. This size of loss meant that even if we disregarded non-cash expenses, such as the $9bn impairment, depreciation, content rights amortization and a drop in the volume invested in content, cash provided by operating activities was $1.8bn, up from $1.38bn in the first six months of 2023, but which was more impacted by content production, accounts payable and the like.

Turnarounds Take Time: Patience and Optimism Required

Trying to be optimistic, there are still some good prospects for Warner’s medium-term. Turnarounds are challenging and usually take some time for strategies to mature. Films, for example, take a few years to produce, and it’s possible that the next ones to be released will achieve a better level of success than the most recent history, such as Joker II and James Gunn’s Superman. Still on the subject of studios, (good) games also take time. Warner’s hit Hogwarts Legacy took five years to produce.

For DTC, this is also true. Netflix (NFLX) took years to build its profitable platform, while Disney (DIS) with Disney+ only managed to make a profit in this division in the last quarter. The guidance is that DTC’s EBITDA should reach around $1bn by 2025, and as the operational indicators are going well, with an increase in subscribers and an increase in ARPU, it seems achievable in the medium term as the initiatives mature. Another thing that could help this division is the bundle with Disney+ and Hulu, something that already seems to be flirting with the consolidation of the streaming segment.

In Q2, relevant steps were also taken on the debt issue. The company repaid $1.8bn in this period, ending up with $3.6bn cash on hand and $41.4bn gross debt, equivalent to a net leverage of 4x. Evidently, this leverage is still high and even with the low cost it should continue to put pressure on the financial result and eventually on cash flow with debt repayments. On the other hand, the repayment schedule for this debt is comfortable, with much of it falling due in very distant years, which may be enough time for management to get operations in order and deliver a sustainable (and even growing if all goes well) cash flow.

After the breakup plan doesn’t work, there is now the idea of selling smaller assets, which can help both to optimize the structure and organization, as well as to deleverage. Among the candidates is the sale of part of the games operation (which has interesting potential in view of IPs such as Harry Potter, Mortal Kombat, and others) and Polish broadcaster TVN.

Warner Stocks May Be Too Risky Right Now

Considering all the information above, it can be seen that Warner Bros. Discovery, however undervalued, is far from being a clear-cut case. Turning the operations around will not be trivial and will require time, good execution of the strategy, and even more resources to invest in optimizing the segments for long-term profitability and sustainability.

With this in mind, a turnaround is possible, but the scenario still seems quite nebulous (or even more than it was), as we don’t know when the DTC segment will be able to offset the decline of the networks, so there is a need to keep in mind that Warner Bros. Discovery seems asymmetrical and could become a value play in the future, but the signs are not yet clear enough to be sure that it is not a value trap.

Based on this, even though I still partially believe in a Warner turnaround (based mainly on its IPs and possible efficiency advances in DTC and Studios), I understand that the risk-return ratio has been changing, and due to the greater risks, I believe that a ‘hold’ rating fits better in this scenario and refers to the caution needed at the present time. I still don’t think Warner will be a value trap, but the turnaround may take longer than estimated, and if the company continues to perform poorly fundamentally and destroy shareholder value, it will be more efficient to allocate new resources to other stocks (with clearer triggers, with the operational more on track and the like).

Read the full article here