“Nothing is as important as we think it is when we are thinking about it.”

– Daniel Kahneman

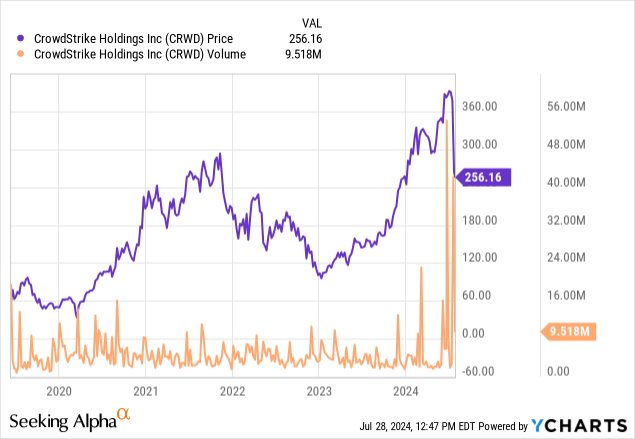

As a brief recap, a bug in an update from CrowdStrike (NASDAQ:CRWD) caused massive outages on Windows this week. As a result, the company experienced a drop of about a third of its price, rating downgrades, price drops, and a conversation on cybersecurity protocols, impacts, and fragility of network systems.

Drastic results in stock prices are hard to evaluate and often create mismatches in fair value prices versus reflected prices. Many investors experience fight or flight responses, which result in unreasonable selloffs in herding behavior or protective stances of their perceived turf, resulting in holding tight a sinking ship.

The difference between these two is whether we are acting on an emotional response, whether this is a sinking ship or one experiencing strong waves.

This article will examine the ship, the waves, and siren calls, among other psychological tricks the sea plays on us, especially in these conditions.

The Sea

Cybersecurity is one of the seven trends that will define the 21st century. It is the central point of the “Data Dilemma,” which involves balancing privacy concerns against the invaluable benefits of data utilization. Until my last portfolio review, I had not found a way to get meaningful exposure to this trend.

For its many flaws, this bug proved CrowdStrike’s reach and impact. While this could be seen as a destructive test, where the proof of its reach curtails it, Microsoft (MSFT) is not reducing the reach or access, which contradicts that assumption and further shows how strong the moat CrowdStrike has built.

The space is not without competitors; this week, Alphabet (GOOG)(GOOGL) was turned down for its $23 billion acquisition of Wiz. While this particular event showcases the importance of cybersecurity and the active competition, it also shows that the market is putting a high premium on the cybersecurity edge, which could be absent in CrowdStrike while the pessimism lasts.

The Ship

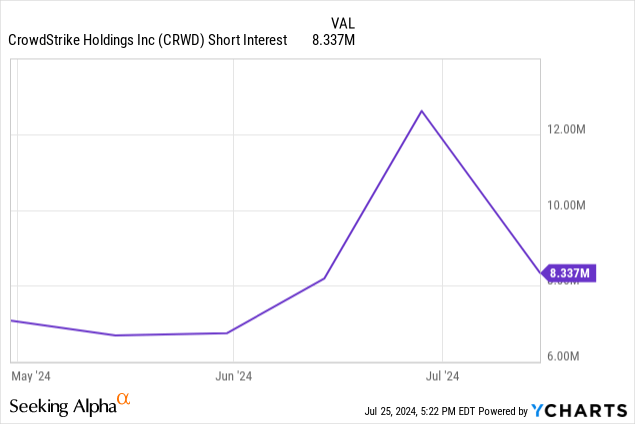

The company had a spike in short interest as the report came in. While the short interest has decreased as the price drops, there is still more short interest than the usual average, which could signal that more pain is still on the horizon.

Following the hit, CrowdStrike, BofA lowered its price target on the stock to $365 from $400 but maintained its buy Rating, HSBC downgraded it from buy to hold $302 from $388, KeyBanc from 420 to 300, and Barclays from 400 to 285.

Even the most pessimistic outlooks are very optimistic versus its current $255 price. This shows that while the street reflected a sharp hit consistent with the price drop, it is still bullish on the company’s medium-term prospects.

This is consistent with IBKR’s most active list, where CrowdStrike landed in third place, showing a buying-the-dip mentality.

Valuation

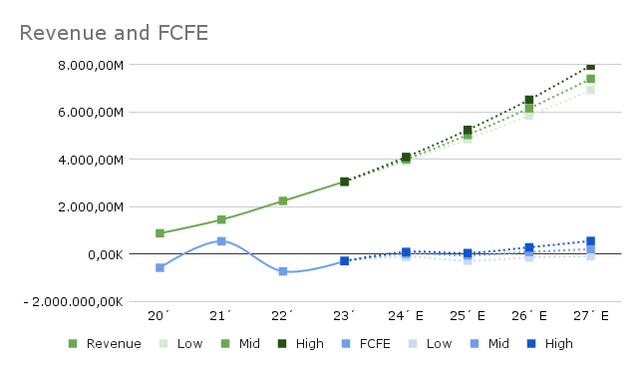

I am reflecting slight variation in revenue expectations in the short term, while those expectations reductions are shown in the long term.

Revenue And FCFE estimates (My Charts)

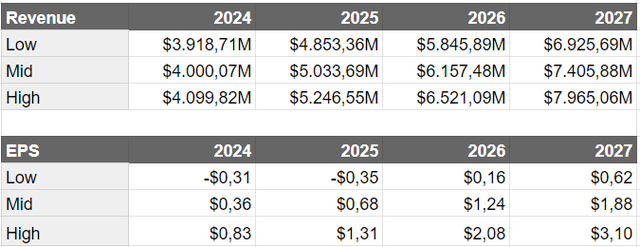

The earnings expectations show only operational results. For example, last year, the company had an EPS of $0.37, while here, it is reflected at $-0.03 to reflect the non-operational interest income that represented around $150 M, among other adjustments.

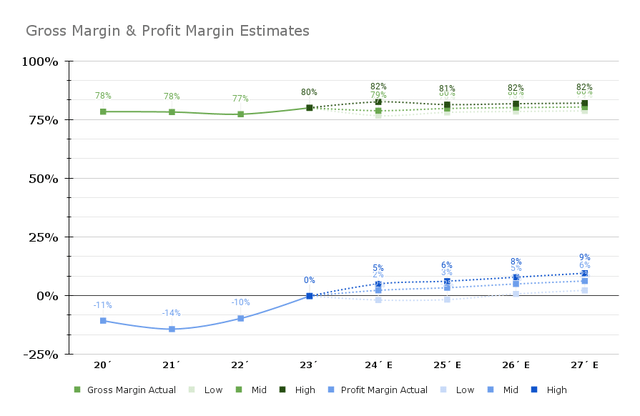

Gross & Profit Margin estimates (My Charts)

The gross margin is forecasted to improve in all cases, but slightly more so on the high range of estimates, and not extremely in any of the cases. Profit margin is a different story; here, we see significant differences between scenarios, with the high scenario reaching almost double digits and the low scenario barely achieving profitability (after adjustments) by 2026.

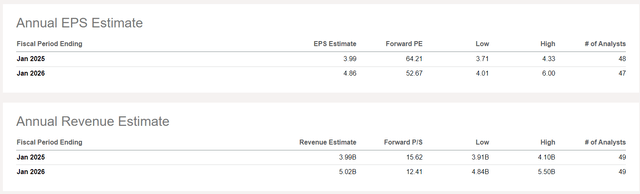

Revenue and EPS Estimates (My Charts)

When comparing my “Normalized” EPS estimates vs the market, we can see that Revenue expectations are in line, but normalized EPS is substantially more pessimistic than reported.

EPS and Revenue Estimates (Seeking Alpha)

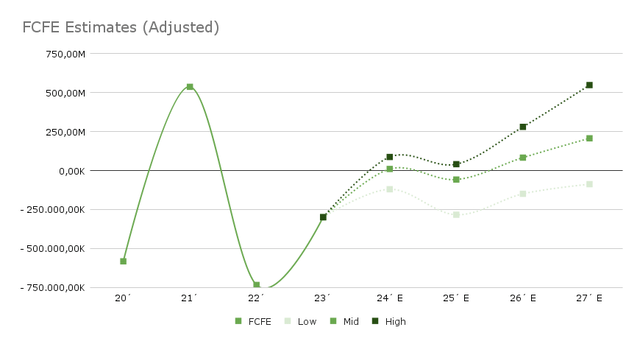

Free cash flow, which is used for the valuation, is still tempered to account for non-operational core business results. The main adjustment is the reduction from Other operational Funds, which mainly consists of stock-based compensation and deferred revenue. This seemed the best choice so as not to overestimate the company’s cash positivity in the short term.

FCFE – CRWD Estimates (My Charts)

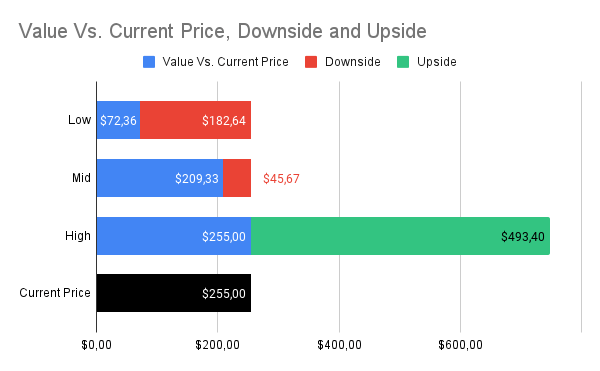

These modifications that reduce EPS and FCFE yield the following values, showing that the high-side scenario upside is gargantuan and consistent with the pre-bug optimistic expectations for the stock. However, we are not there anymore. The stock mid-scenario still has some legroom to drop, while it would be severely overvalued in the low scenario. This reflects its inability to scale in the same way it has been able to do so thus far.

Fair Value estimates (My charts)

For now, it is hard to put a new optimistic side of the stock, as the dust has not settled. So, while it is interesting to see where the past optimistic range was, we need to focus on the mid and low scenarios.

Syren Calls

There are two very distinct groups in this situation: Group 1, those caught holding the stock, and Group 2, those who now see it as an opportunity.

Those caught holding the stock typically experience fight-or-flight responses, which trigger a selloff or irrational holding. Those seeing this as an opportunity must evaluate whether this is a falling knife situation or a “once in a lifetime” opportunity triggered by an unjustified selloff, and the Fear Of Missing Out is ever-present.

The volume spike seems impressive. However, the shares traded these days were around 160 Million, around 65% of the shares outstanding. This is a large number, but even if all shares were only traded once, this signals a strong confidence of the original stockholders. The fight was chosen much more than flight.

This signals confidence in the stock, which is positive; however, this confidence could still dissipate, bringing the stock lower. Current holders are likely experiencing a level of regret about not selling sooner, and this mentality often results in a “getting even” mentality. This is when arbitrary prices are set for selling the stock, like “when it reaches the price I bought originally” or “when it reaches where it was when the bug happened.”

It is impossible to know how prevalent this feeling is among current holders. Still, given the sharp and sudden drop in the stock and the relatively low float, my wager is that the holders are having a more emotional than rational response.

All this is key to evaluating our options in Group 2. Understanding the key figures gives us a much clearer picture of how solid the ground is and the type and nature of volatility the stock could have.

The only other caveat that might not be as relevant given the “small” short interest is the dead cat bounce. When short sellers buy stocks to close their positions, stocks might show a jump in their prices. Many confuse this event with a rally, and the emotions of FOMO run wild.

Conclusions

It would appear that CrowdStrike’s moat is strong enough not to be destroyed with one blow. The confidence of key customers and holders is encouraging, and the fair value is relatively close to current price levels. However, the lack of a short-term catalyst, the above-average short interest, and the relatively low trading volume (for such an extreme situation) may signal a slow recovery.

This might be a solid stock, but it is still priced above its arguable fair value. Considering this, there are many strategies to build a position and more than enough reasons to walk away.

Let’s look at the Tortoise and Cat portfolio outlook.

The Tortoise portfolio: True to its family motto, it would wait and see. Yes, the stock is attractive, and cybersecurity is a key trend for the following years, but it is not the only player, and the key priority of lowering the maximum drawdown is not met at the current price and conditions.

“Good things come to those who wait”

At a longer price, it could be considered after a plan to get back on track is clearly detailed and the guidance is cemented. While these conditions likely would imply a higher price than what the stock currently has, the risk-averse portfolio has no issue paying a premium for reduced risk rather than suffering volatility.

The Cat portfolio Would jump fully to a position, with a protective Put in place. FOMO is the design flaw of this risk-seeking portfolio, but it is protective and nothing to neglect. The portfolio recognizes the instability of the stock and the risks it faces in the short term. This strategy mitigates the FOMO and is long on the Volatility the stock could have either way.

For my portfolio, I will use my valuation to guide the decision. With the valuation used, I believe the stock’s fair price is around $240-$245. Conscious of the risks and alternatives, I would rather wait and get a half position if it reaches this range and completes the position if it reaches much lower, with its growth prospects intact, or if it jumps on a clear path due to reduced uncertainties and lowered risks.

Returning to one of my favorite Charlie Munger quotes.

The big money is not in the buying or selling, but in the waiting.

– Charlie Munger

The stock will be interesting this week, and waiting a little longer seems like the smart choice. Waiting is betting the current holders run out of patience, the stock does not rally (outside of a dead cat bounce), and a better opportunity will occur to purchase the stock or gain exposure to the cybersecurity trend.

Read the full article here