Overview

We rate Global Ship Lease, Inc (NYSE:GSL) a Hold to Moderate Buy opportunity. Earnings and revenue are strong. Cash flow from operations is healthy. Our rating hesitancy stems from the shares selling near their 52-week-high. Moreover, the economy, the Fed, and market dynamics appear, as the Principal Financial Group poignantly describes on Seeking Alpha, to be standing on “shifting sands.”

On the upside, the dividend yield offers a good return. Management is reinvesting capital in the company. However, there are risks. Ominous geopolitical portents for the shipping industry loom. We were more enthusiastic about the industry earlier in the year when we saw a buying opportunity for A.P. Møller Maersk (AMKBY) and rate increases for the shipping industry.

Profile

Global Ship Lease is the owner/operator of 68 mid and small containerships. The firm is benefitting from rising shipping rates and demand for space. There is a worldwide shortage of containers. The dividend yield tops 5%. Global is positioned, in our opinion, to benefit greatly from steady increases in maritime volume expected over the next two decades, but other analysts are forecasting lower earnings per share in 2025 and 2026.

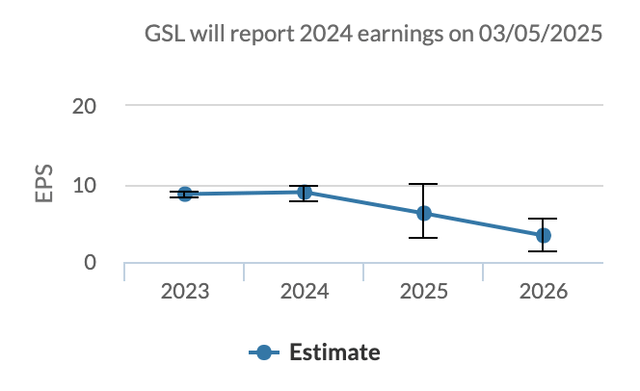

Earnings Estimates (Market Watch)

The company was founded in 2007. It is based in Greece and incorporated in the Marshall Islands. The corporation has undergone several restructures. Seeking Alpha reports, hedge funds own 5.6% of the ~38M outstanding shares. Institutions and the public each own about 43.3%. Corporate individuals/insiders own a hefty 7.47%. We like the transparency and wealth of information Global’s management shares on its first-class, easy-to-maneuver, home site.

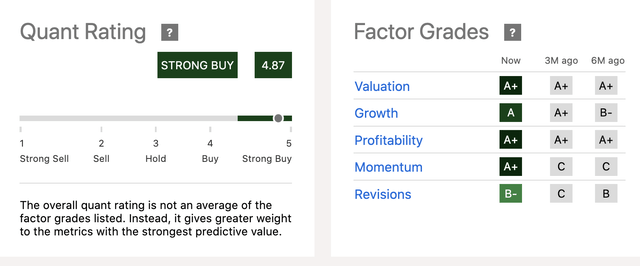

Quant Rating & Factor Grades (Seeking Alpha) Quant Rating & Factor Grades (Seeking Alpha)

Three credit-rating agencies upgraded the stock in June ’24 after the company’s strong Q1 ’24 release. GlobalNewswire highlighted the upgrade,

The Company’s significant progress deleveraging, its focus on maintaining a disciplined, low leverage strategy, and revenue stability based on attractive multi-year time charter agreements. The agencies also cited GSL’s strong earnings and cash flow profile through market cycles, as well as robust counterparty credit quality. Additional key considerations included the Company’s experienced management team and strategic positioning, in particular its focus on medium-sized and smaller containerships, with value-added components such as high reefer capacity.

Container Shipping Market Overview (Bimco)

Financial Management

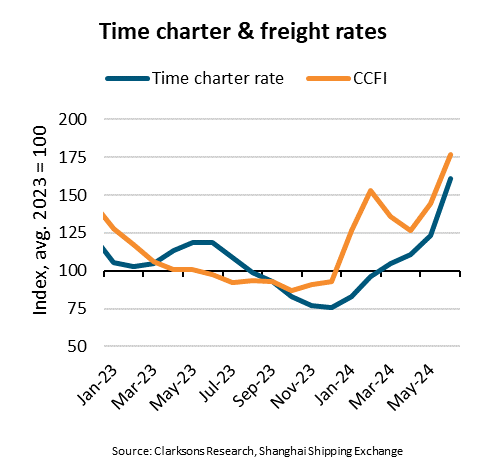

The maritime shipping industry recovered since the pandemic. Container and shipping rates dropped after spiking. Headwinds worry economists as shipping rates are increasing from sputtering economies, war in the Middle East, and terror attacks on ships. Time at sea is extended. Tariff wars hurt imports/exports. Since 2021, ships can sit near harbors waiting for days and weeks to dock and unload.

These and other problems are stimulating rate price increases. To contain costs, shippers are turning to companies like Global Ship Lease. They are chartering more container ships for longer periods. Seatrade Maritime estimates charters are extending out on average 24 months, while 36 months charter leases are appearing.

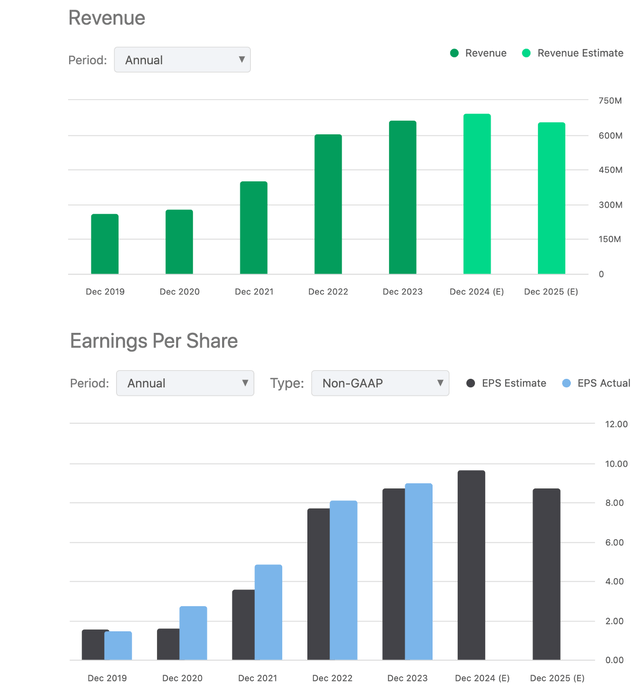

Global Ship Lease’s revenue climbed since 2020 reflecting how the company capitalized on the maritime stresses. Revenue jumped from $282.3M in FY ’20 to $666.7M in ’23. Concomitantly, gross profit was $168.3M in ’21 and $463.9M last year. Earnings from operations increased nearly 7.4xs from $41.6M in FY ’21 to $304.5M in ’23. Cash flow from operations steadily rose each year to $375M.

Revenue & Earnings (Seeking Alpha)

Based on past EPS and guidance from management, we forecast an FY ’24 EPS in the range of $9.45 to $9.70 compared to the EPS of $9.03 in 2023. Higher earnings will depend on revenue growth above 11% in 2024 and the company’s ability to maintain its high gross profit margin in the 60% range. Last year’s second quarter EPS was $2.09 per share; we forecast Q2 ’24 EPS will be about $2.35. The company beat EPS forecasts in 7 of the last 8 quarters.

Other positive news for investors is that hedge funds increased their holdings in the last quarter by ~970K shares. The number of hedge funds owning shares since Q2 ’23 jumped from 12 to 18 at the end of Q1 ’24.

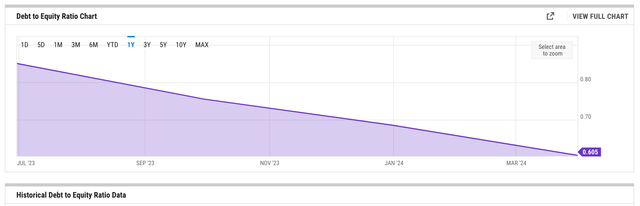

Debt at last report is $500.7M down from $540.3M at the end of 2023 and $637.3M closing FY ’22. The debt-to-equity ratio has been improving over the years:

Debt-to-Equity (YCharts)

Cash is up Y/Y and the company is committed to reinvesting capital at nearly three times the rate earned in the industry. Multiplying the PE ratio of 2.98 x $9.68 EPS, the fair value for the stock is $28.84. The fair value share price tops $31 employing a PE ratio of 3.25 where some analysts suggest it currently stands.

Valuation

Seeking Alpha’s Valuation Factor Grade is A+ with a strong buy Quant Rating. Global Ship Lease beats the Industrials in virtually sector median category:

- The Industrials sector median of 19.05 for P/E non-GAAP (TTM) compares to Global’s at 3.05.

- The Enterprise Value to EBITDA is 12.71 to Global’s 3.53.

- The Price-to-Sales ratio is nearly equal, but Global’s Price-to-Book is 0.8 versus the Industrial’s 2.73.

- Global’s Price-to-Cash Flow is significantly better than the Industrial’s sector median.

- Global’s Dividend Yield of 5.2% beats the sector median of 1.42%.

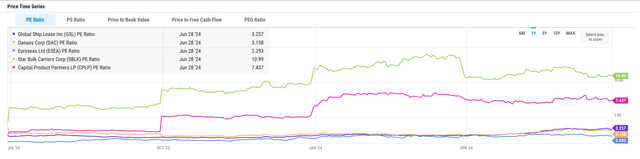

- Shares of Global are up 51% over the last 12 months and 45% YTD, while SonciShares Global Shipping ETF (BOAT) shares, a leading ETF in maritime shipping, are up 42% in the last year and 22% YTD. Global has momentum in all price categories.

Price Time Series (YCharts)

The company’s market cap is up +60% over 3 years, now topping $1B. Earnings growth over the last decade exceeds 136%, and the PE dropped from 5.8 to about 3.

Risks

The primary risks for investors are the hot wars dragging on and spreading. They will greatly hinder maritime shipping. The cold wars turning hot between Israel and Hezbollah, China and Taiwan, and China and the Philippines is worrisome. The shipping industry, like the Merchant Marine during World War II, can become an easy target.

Despite Global Ship Lease paying down debt, there is a lingering risk to shareholders. Cash and receivables at the last report total $215M, but current liabilities top $266M. An immediate concern is offset by Global’s net to EBITDA 1.0 ratio and that interest expense is well-covered by EBIT. Shareholders can be diluted if the noise about possible sputtering economic growth and belt-tightening turns into banking demands for cash.

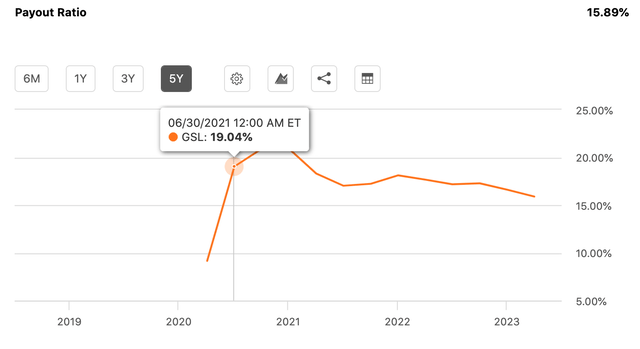

The dividend safety rating is not top-notch; the payout ratio and consistency are low. The growth rate gets a D- Factor Grade. The next earnings release is scheduled for August 1, 2024.

Dividend Payout Ratio History (Seeking Alpha)

The stock has a low leveraged/unleveraged Beta rate of 0.40, but short interest is climbing; it is up to 7.55% from 5.7% a few days earlier.

Takeaway

We came upon Global Ship Lease, Inc. too late to deliver an enthusiastic stock assessment. We do not foresee a particular event that will raise the share price significantly; it is already selling at a fair value after climbing last year and YTD. Investors can benefit from watching moves in and out of the stock by hedge funds over the next 6 months. Geopolitical factors will affect the stock price. The dividend yield is attractive, but not ensured. If you own it, we believe the stock is worth a Hold Rating or perhaps a moderate buy opportunity to dip in price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here