Investment Thesis

The semiconductor complex of stocks has been a huge beneficiary of the AI wave that has lifted business spending in the semiconductors and chips industry, especially by large technology firms and hyperscalers, large cloud providers such as Microsoft (MSFT), Meta Platforms (META), Alphabet (GOOG), etc.

Semiconductor companies are spread across the value chain of the industry, largely in three stages of the chip-making process: Design, Manufacturing and Packaging. Nvidia (NVDA) is currently the most popular semiconductor company because of the meteoric ascent demonstrated by the company after the market slump in 2022. This has also boosted the fund performance of the VanEck Semiconductor ETF (NASDAQ:SMH), an investor-favorite ETF, which has almost a quarter of its assets allocated towards Nvidia.

However, I believe there are other companies in the semiconductor value chain, such as Taiwan Semiconductor Manufacturing (TSM), Broadcom (AVGO), and Qualcomm (QCOM), that are part of the SMH fund and have equally bright prospects, enough to keep the momentum in SMH alive.

I recommend a Buy rating on SMH.

About the VanEck Semiconductor ETF

Offered by NYC-based asset management company VanEck, the SMH ETF is aimed at investors who are looking to gain exposure to the semiconductor industry. In my last coverage of the fund, I explained details about its composition and structure, and I also noted how the fund deploys capital into the largest and most liquid semiconductor companies listed in the U.S. markets.

The fund continues to achieve its objective of offering investors exposure to the semiconductor industry by tracking the market cap-weighted MVIS® US Listed Semiconductor 25 Index.

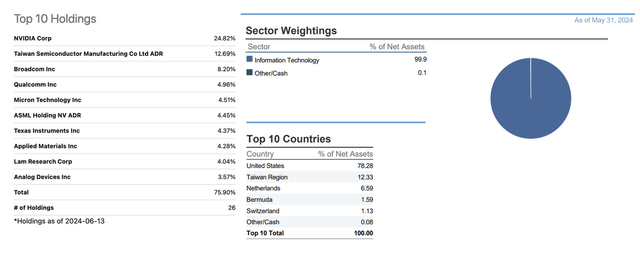

In Exhibit A, I observe the top 15 holdings vs. breakdown of the fund’s assets by sector and other factors.

Exhibit A: Top 10 holdings for the VanEck Semiconductor ETF (Various sources)

Peer Comparison

Comparing SMH to its largest peers, the fund dominates its peer group on a performance basis as well as by assets managed, as can be seen in Exhibit B below.

Exhibit B: Comparison of semiconductor-focused etfs by various fund metrics (SA, Google finance)

SMH, iShares Semiconductor ETF (SOXX), the erstwhile semiconductor ETF leader by market cap, as well as SPDR S&P Semiconductor ETF (XSD), compete head/head with each other on ETF fees. Invesco’s PHLX Semiconductor ETF (SOXQ) competes directly with SOXX since both of these funds are structured on the Philly Semiconductor Index (SOX). I have covered the SOXQ ETF and SOXX ETF recently.

But as I mentioned earlier, SMH has delivered monster-sized gains due to its outsized exposure to Nvidia, as demonstrated in Exhibit B. So far, the underlying MVIS® US-Listed Semiconductor 25 Index’s massive weight to Nvidia as well as exposure to other weighted components, as shown in Exhibit A, have benefited SMH since it tracks the MVIS Semi index.

Broadening AI spend & changing business spending preferences should benefit non-Nvidia names

In my previous coverage on SMH, I had explained long-term trends remain but was looking for further confirmation in Nvidia’s Q1 FY25 earnings report. Since my coverage the fund has surged 33%, while Nvidia had a stellar quarter. On the Q1 FY25 earnings call, management explained how demand was broadening out into other products such as their data center networking products as well as other verticals.

Nvidia has been one of the faces of the AI revolution, as companies quickly pivoted towards procuring the company’s GPUs for upgrading their back-end data centers. The sudden demand led to Nvidia being an overnight beneficiary, with its revenue doubling over the past year while its net income more than quintupled during the same period.

I believe the spending over the past year points to AI spending being in its formative years, and cloud companies, technology companies, & AI startups will also look to expand their capabilities by continuing to expand their data centers, while some hyperscalers are also looking to wean off their dependence on Nvidia by designing and manufacturing their own chips.

In scenarios like this, Nvidia will still stand to benefit due to its massive +90% market share in the datacenter GPU market, but other companies in the semiconductor value chain will also benefit as data center spending broadens. Here is an example of what the value chain looks like today and some of SMH’s components that are part of this value chain.

|

Design |

Manufacture |

Full Stack Semi Companies |

|

Fabless: Nvidia, AMD, Broadcom, Qualcomm |

Foundries: TSMC |

Intel (INTC), Micron (MU), Analog Devices (ADI), Texas Instruments (TXN) |

|

IP & Design: Synopsys (SNPS), Cadence (CDNS) |

Equipment: ASML (ASML), Lam Research (LRCX), Applied Materials (AMAT), KLA Corp. (KLAC) |

Increased demand vectors for AI and data center infrastructure will continue to lift Nvidia, Broadcom, & AMD. Data center spending is now expected to surge 10% in 2024 after growing just 3% in 2023. Most of the spending is expected to be led by hyperscalers, who are expected to spend ~$200 billion in 2024, but research suggests this figure will grow to $1 trillion by 2027. Plus, other end-user segments, such as AI PCs, are expected to grow as AI PCs increasingly account for a major share of PCs shipped around the world. The demand is already showing in AI smartphones, with Samsung’s S24+ phone shipments growing by 53% over last year.

Both AI PCs and AI smartphones will run on Qualcomm’s and AMD’s latest chips, which are designed and manufactured by companies in the value chain I listed above in the table. Here is an excerpt from Broadcom’s recent earnings call, where their management indicated that their spending outlook on their semiconductor products will continue to be strong:

Q2 revenue of $3.8 billion grew 44% year-on-year, representing 53% of semiconductor revenue. This was again driven by strong demand from hyperscalers for both AI networking and custom accelerators. It’s interesting to note that as AI data center clusters continue to deploy, our revenue mix has been shifting towards an increasing proportion of networking.

Talking of AI accelerators, you may know our hyperscale customers are accelerating their investments to scale up the performance of these clusters.

Such a strong spending outlook is also expected to lift semiconductor manufacturing companies like TSMC, which manufactures chips for fabless companies like Nvidia, AMD, and Broadcom, which design the chips. Most of these companies also utilize design software provided by Synopsys or Cadence. Synopsys and Cadence operate in an oligopolistic market for design software and IP, where they both hold three-fourths of the design market, which is expected to grow ~13–15% CAGR over the next five years. I have covered this in detail in my coverage of Cadence in the past.

Full-stack semiconductor companies like Micron that design, manufacture, package, and sell their computer memory and storage products are also benefiting from a boost as demand for memory products surges. Micron is also seeing sustained momentum despite raising the price of its memory chips.

All the companies that I discussed are part of the larger growth story playing out in the semiconductor space and are all components of the SMH fund.

Outlook and Valuation

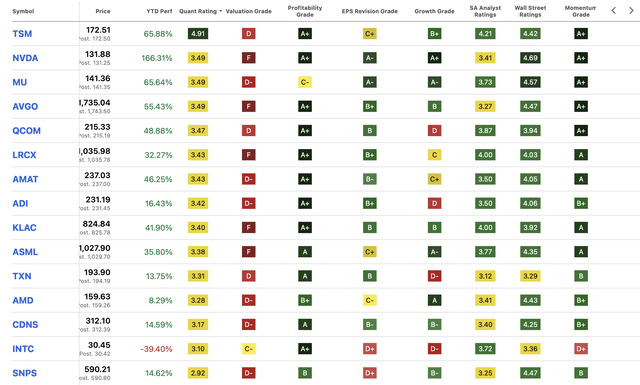

Currently, most of the components in the SMH fund look overvalued if I compare the companies in the fund by their Quant Ratings metric provided by Seeking Alpha, as seen in Exhibit C.

Exhibit C: Comparison of semiconductor-focused etfs by various fund metrics (SA Quant Ratings)

Upon further inspection, these companies have lower Valuation Grades since they have enjoyed momentum, as indicated by the Momentum Grade. EPS revisions still look favorable and point to some bullishness still persisting.

According to Morningstar, the fund currently commands a PE of ~29x, which is pricey. But with earnings still expected to grow 35–40% over the long term, I still believe SMH has enough runway to grow from here.

There may be a pullback in the fund due to the massive runup this year, but I believe that would present investors with an opportunity to initiate or add positions in the fund. Investors may also wait for a pullback to the 50-day mark to deploy capital to the fund.

Risks & Other factors to look for

Most semiconductor companies benefit from the increasing capital expenditures of technology firms that capitalize on semiconductor products. Therefore, it is important to track the capital expenses of technology firms and other customers, which indicate the outlook on sales for semiconductor companies. I had mentioned earlier how capex is supposed to grow at a 38% CAGR to $1 trillion by 2027. Additionally, research by some leading economists also points to a booming capex environment, which will continue to be beneficial for semiconductor companies that are part of the SMH fund.

If the customers of all semiconductor companies start to experience slowdowns in their respective revenue streams, these technology firms will in turn start to slow down their capex forward spend outlook, which will create headwinds for semiconductor companies and pressure their performance. This, in turn, could also pressure the performance of the SMH ETF.

Takeaways

The semiconductor complex of stocks remains one of its strongest cycles of growth as AI continues to provide an uplift in the outlook for these stocks. Nvidia has seen its market cap multiple over the past many months, and in the next leg of AI spending, I expect other companies such as Qualcomm, Broadcom, and Micron to add to the growth story of the SMH fund. The valuation looks pricey in the short term, but with the immense potential the companies in the SMH fund hold over the long term, I believe the SMH fund is a Buy.

Read the full article here