Adobe Inc. (NASDAQ:ADBE) investors received a much-needed respite last week as the creative software company reported its earnings. Adobe’s second fiscal-quarter earnings release brushed aside the market’s pessimism, as Adobe posted a beat-and-raise quarter. I provided a bullish ADBE update in March 2024, highlighting why pessimism in ADBE could have peaked.

However, ADBE buyers were nowhere to be found as the downward volatility continued in earnest. Salesforce’s (CRM) disappointing guidance led to a sharp selloff across software stocks as investors turned wary over the near-term AI monetization potential of SaaS companies. Therefore, optimism in Adobe’s earnings commentary is welcome, as management underscored its confidence in integrating GenAI. Despite that, Adobe didn’t telegraph GenAI-specific revenue metrics. However, management is confident that deeper integration of Generative AI tools into Adobe’s product platform should continue driving engagement further.

As a creative software company with a well-diversified enterprise and SMB customer base, I would have expected ADBE stock to be more resilient. However, investor fears about a potentially slower adoption of Generative AI services likely impacted ADBE’s buying sentiments (pre-earnings). Therefore, Adobe management’s assurance is timely, as dip-buyers likely assessed the market was too pessimistic on ADBE stock.

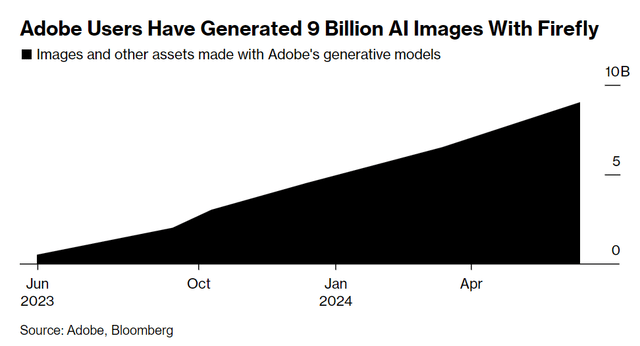

Adobe Firefly AI image generation (Bloomberg)

As a reminder, management updated that the Adobe Firefly AI model has generated more than 9B images over the past year. In addition, Adobe has incorporated Firefly into its essential products, including “flagship products like Photoshop, Illustrator, Lightroom, and Premiere.” Consequently, it is expected to “broaden Adobe’s appeal across different customer segments, including creators, communicators, and businesses.” In addition, the company’s introduction of Acrobat AI Assistant on Adobe’s Document Cloud is expected to “boost document productivity.”

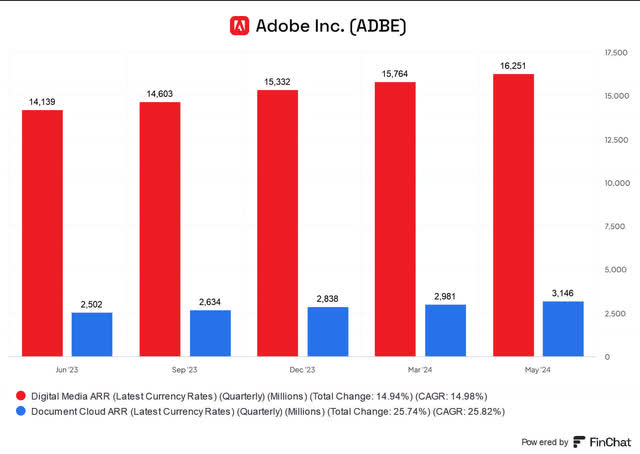

Adobe ARR metrics (FinChat)

Given the significant scale of Adobe’s Digital Media ARR, I expect the market’s focus to remain on Adobe’s creative product suite. In addition, Adobe’s Digital Media segment is assessed to account for almost 80% of ADBE’s sum-of-the-parts valuation, corroborating my observation.

Adobe also indicated that it has broadened customer access to third-party AI models “to offer customers more comprehensive tools.” Therefore, I assess that Adobe has increasingly positioned itself as an aggregator of AI models while providing access to its proprietary models. It demonstrates the versatility of Adobe’s market-leading platform in attracting “strategic partnerships” from collaborators keen on leveraging Adobe’s highly-prized creative customer base. As a result, I believe that Adobe has proven its ability to continue improving its value proposition for its customers by “focusing on delivering personalized experiences at scale.” It should assure investors about Adobe’s ability to fend off potentially disruptive attempts by AI startups.

Recent reporting on these AI software startups highlights the sustainability challenges afflicting more AI startups. In particular, Stability AI CEO Emad Mostaque left in March 2024 amid key staffing departures. Stability AI is one of the more prominent fledgling AI companies that are challenging Adobe’s dominance. However, Stability AI reportedly faced liquidity issues as the company sought to raise funds. It seems like AI startups could be facing a moment of reckoning as the market seeks validation from them to justify their business model.

As a result, I believe these uncertainties should underpin investor confidence in the resilience of Adobe’s fundamentally strong business model. Customers and investors will be increasingly wary of the “story” underlining these AI startups’ value propositions.

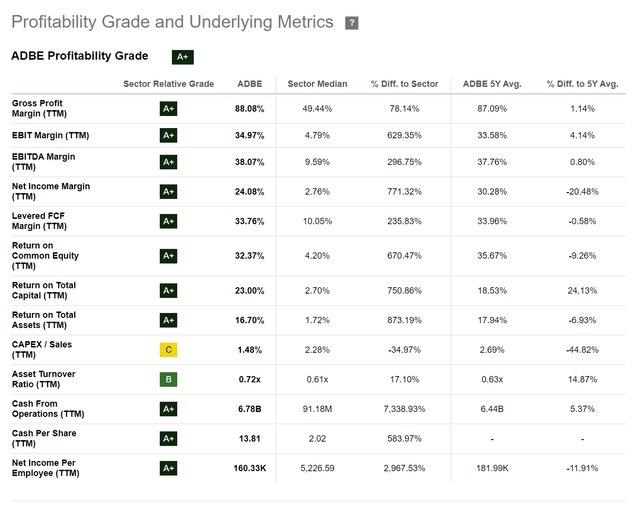

ADBE profitability grade (Seeking Alpha)

As seen above, ADBE boasts a sector-leading profitability grade, highlighting a highly robust business model. Adobe’s platform moat will likely be strengthened by the upheavals experienced by the AI startups looking to disrupt Adobe’s creative leadership.

In addition, Adobe’s ability to act as an AI models aggregator will likely deepen its appeal to its customers, providing flexibility within Adobe’s platform. Therefore, it is expected to strengthen Adobe’s switching costs against potential disruptors struggling to justify their commercial viability.

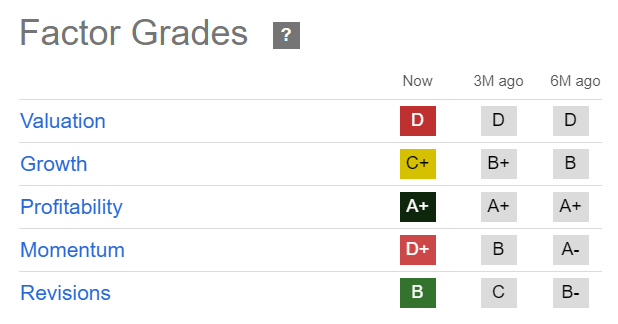

ADBE Quant Grades (Seeking Alpha)

ADBE is assigned a “D” valuation grade, which suggests it’s still priced for growth relative to its peers in the tech sector. However, ADBE’s forward adjusted PEG ratio of 1.68 is more than 15% below its sector median. Therefore, I assess that sufficient pessimism has been priced into ADBE’s growth prospects bolstered by its fundamentally strong business model.

Nevertheless, the lack of robust buying sentiments in ADBE (“D+” momentum grade) suggests investors must still be prepared for downside volatility. The market could remain cautious as Adobe navigates the integration of GenAI into its product ecosystem.

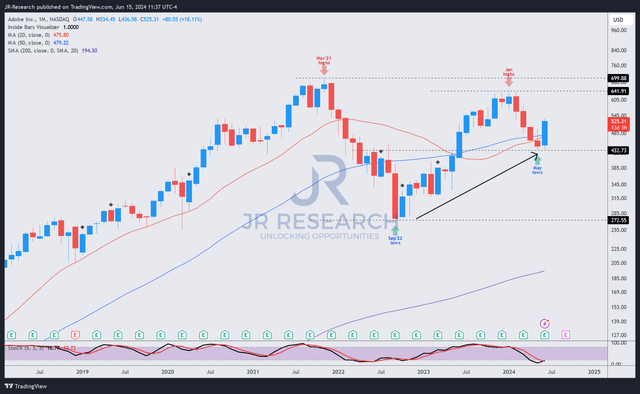

ADBE price chart (monthly, long-term) (TradingView)

ADBE’s price chart suggests that its long-term uptrend bias has remained intact. Therefore, ADBE’s pullback from its January 2024 highs has not invalidated its long-term bottom formed in September 2022.

As a result, ADBE seems well-poised for further recovery. Dip-buyers returned aggressively last week, helping it stage a remarkable rally above the $430 level.

I assess that as long as ADBE’s $430 support level holds robustly, it should provide confidence for more buyers to return and partake in ADBE’s bottoming opportunity.

Rating: Maintain Strong Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing, unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here