By Carol Lye

Japan has been struggling for some time to generate enough velocity in inflation to escape the gravitational pull of deflation. We had written last year that a liftoff from Japan’s negative interest rate policy (NIRP) would be a story for this year. That view was based off the belief that core inflation would meet the Bank of Japan’s (BOJ’s) target. As anticipated, NIRP was removed at the March BOJ meeting. So where does Japan go from here?

The story for the rest of 2024 and into 2025 is now centered on whether inflation will be sustained at the BOJ’s 2% target. If so, that would affect the number of eventual interest rate hikes from the BOJ. It is prescient then that Deputy Governor Uchida mentioned “this time is different” in his speech at a recent conference held on monetary policy developments.

Sustained Inflation Going Forward?

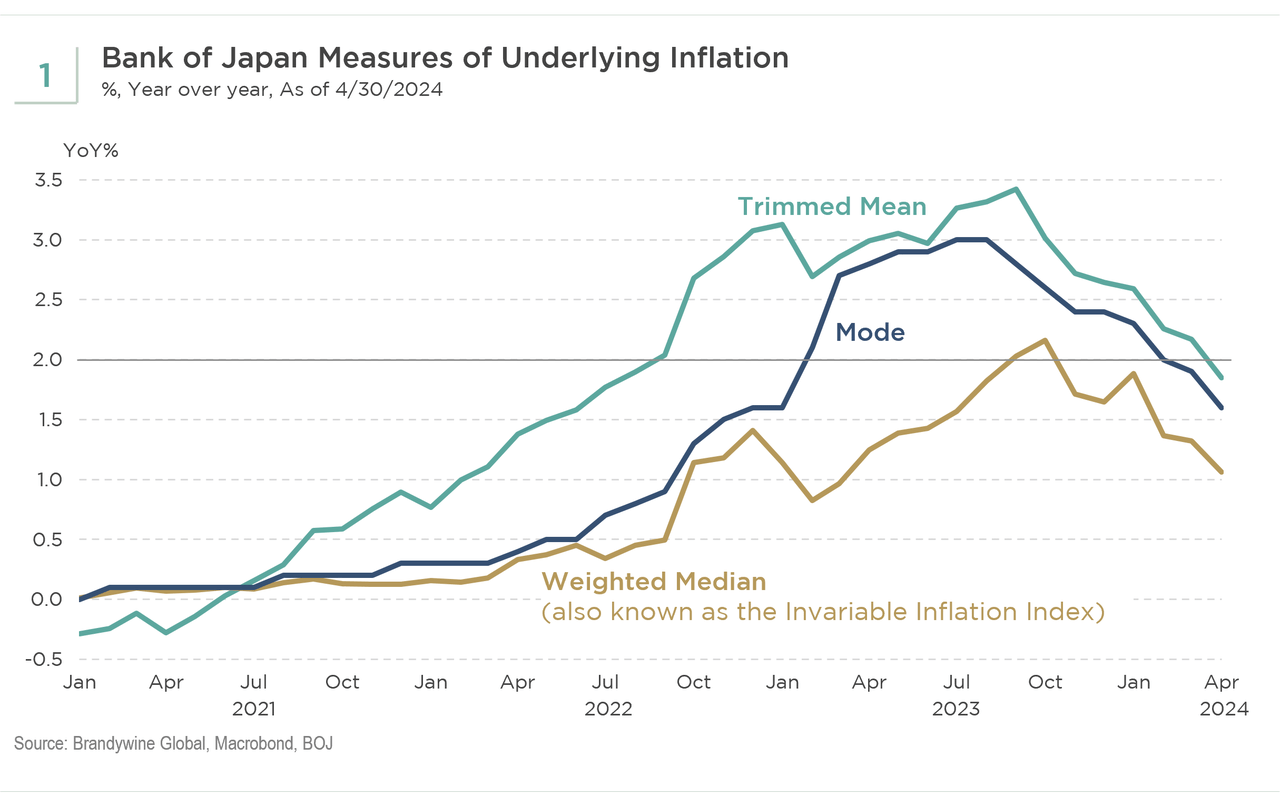

Many seem to have given up hope on ever seeing sustained inflation in Japan. The recent trimmed mean inflation numbers seem to suggest that inflation is rolling over (see Exhibit 1). However, that might not be the case if one looks into the details. The details suggest that going forward, inflation might just be accelerating again, pushing Japan entirely out of the deflationary orbit.

Hidden Inflation Boosters

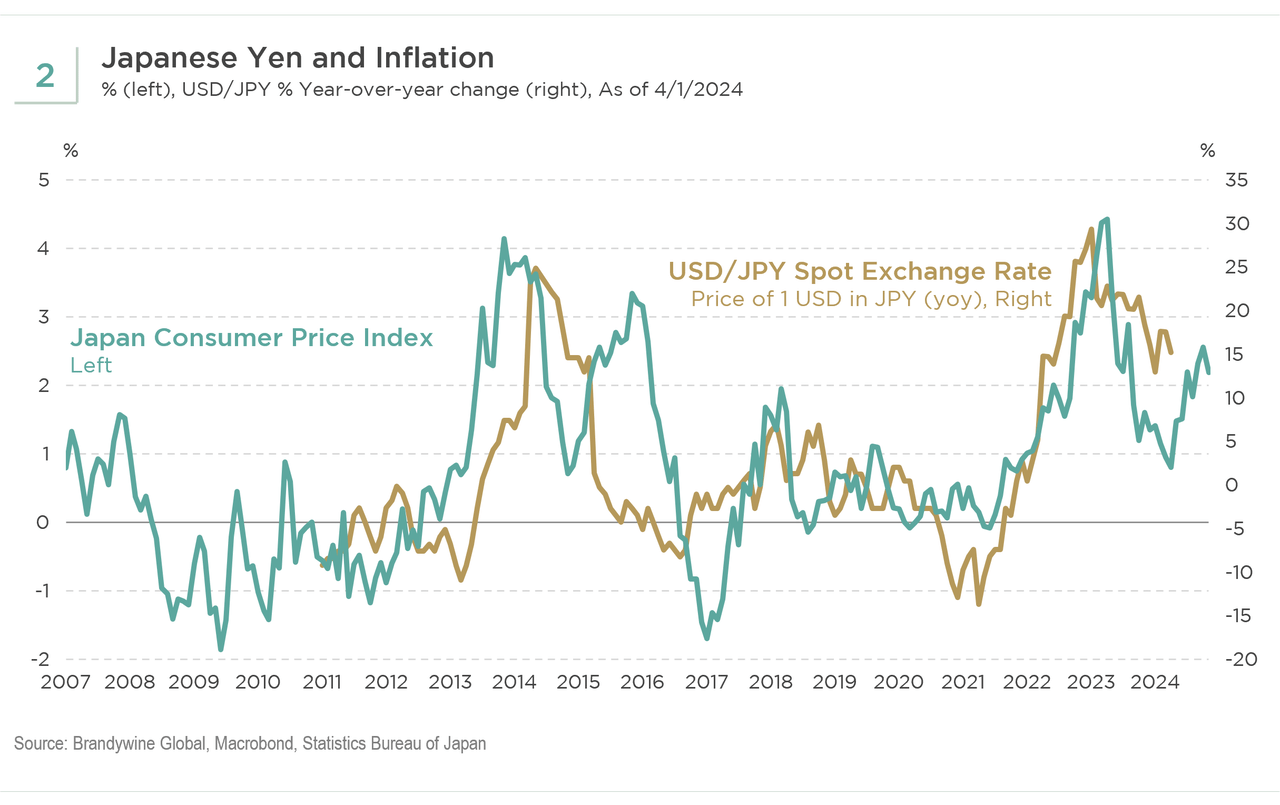

First, on the goods side, the yen has been extremely weak. That weakness has been driven partly by the wide interest rate differential between the U.S. and Japan. Related to inflation pressures, this weakness in yen creates a feedback loop into the economy, which is resulting in higher import prices (see Exhibit 2). The recent Economy Watchers survey shows Japanese corporations are increasingly concerned about the high import prices due to the weak yen, which reduces their profit margins. And this concern also has caught the attention of the BOJ.

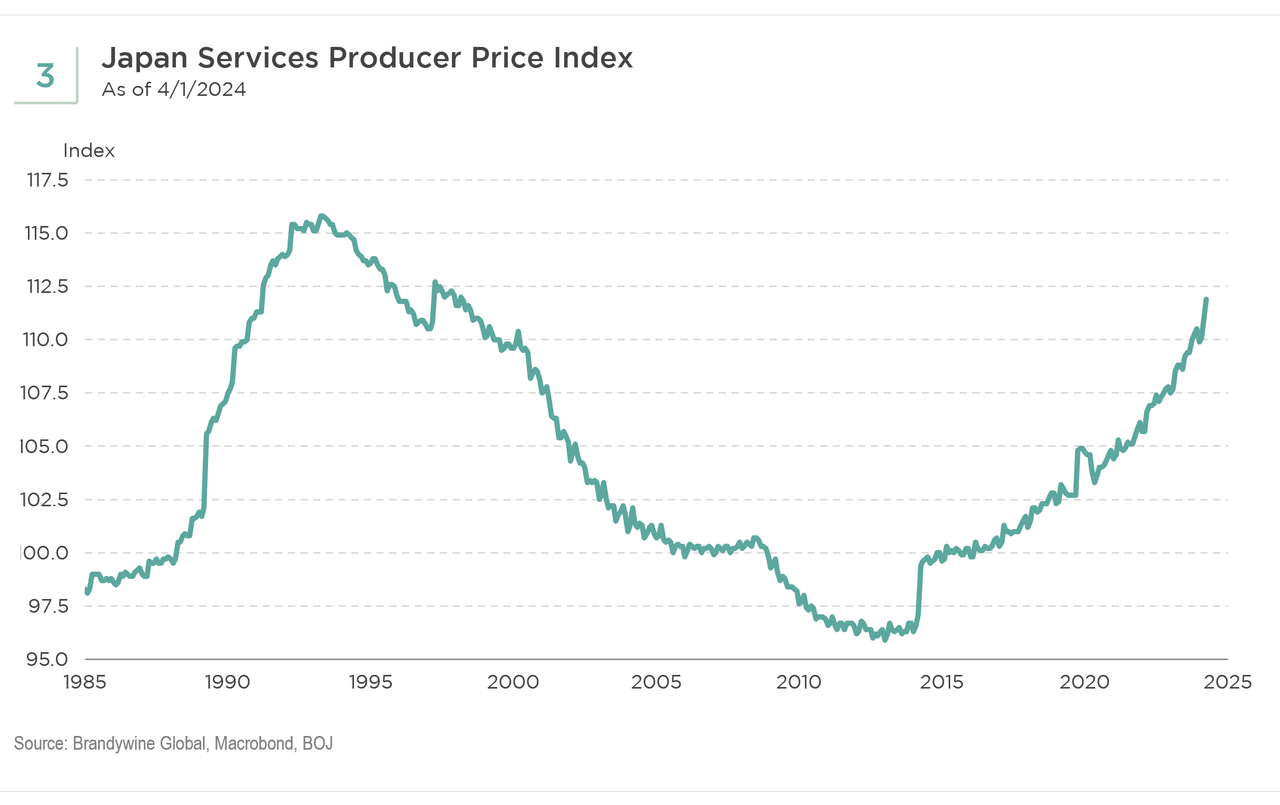

On the services front, it is well known by now that the 2024 spring wages are being revised up by an average of 5%. This wage growth has been achieved in the face of some government pressure but also, most importantly, due to a tight labor market. The services Producer Price Index has been moving up and is now at its highest level in 26 years (see Exhibit 3). Real consumer spending in Japan has been weak since 2022 because of higher inflation. But these higher wages could possibly lead to higher consumption. In the past month, a Morgan Stanley report showed domestic department store sales to Japanese shoppers saw a jump, and luxury sales are picking up. Additionally, according to Nikkei Asia, Tokyo and Osaka are experiencing the sharpest rise in condominium prices. The wage-consumption-price feedback cycle may take some time to come to fruition, but it is now more plausible than before.

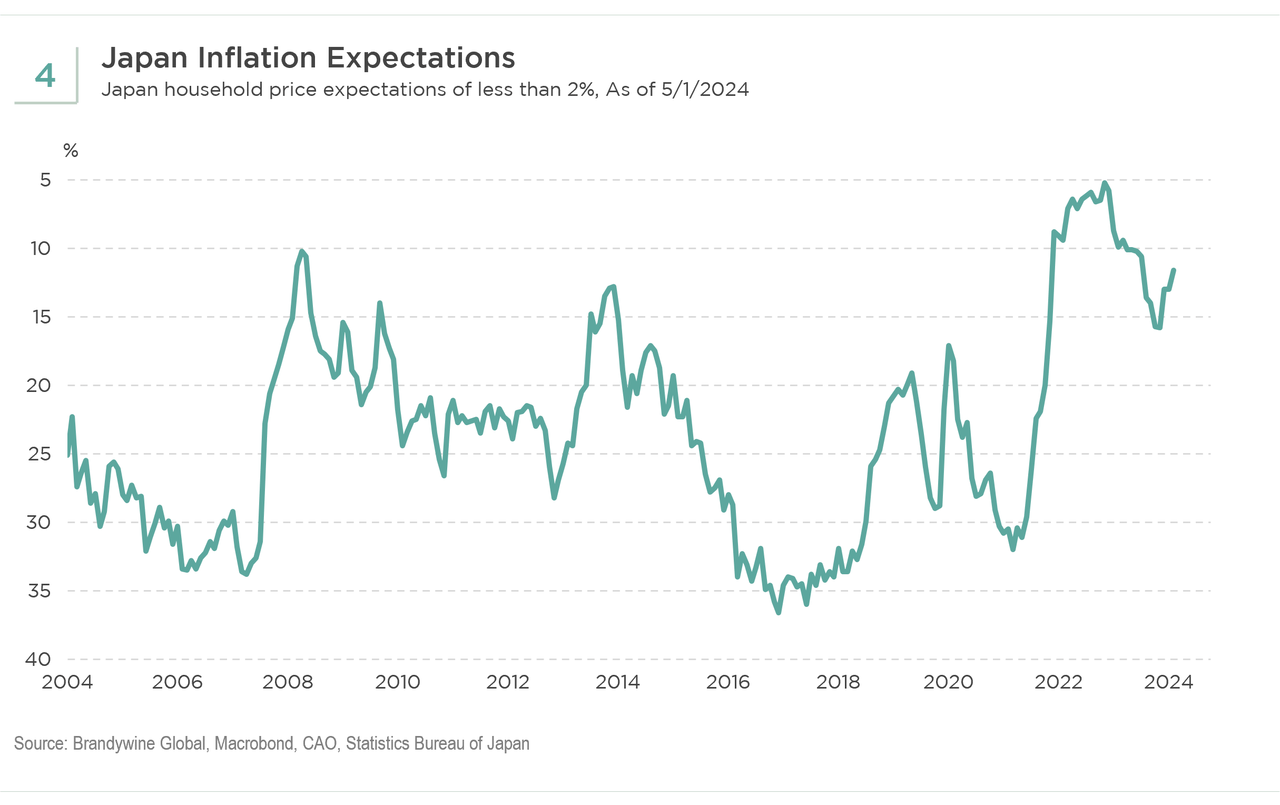

Lastly, the BOJ keeps a keen eye on inflation expectations. It believes that inflation expectations need to be anchored at 2% so that inflation can be sustained. While there may be ingrained or lingering doubts about the sustainability of inflation given the BOJ’s long track record of undershooting its target, recent inflation expectations are indeed suggesting it is anchored at 2% (see Exhibit 4).

Implications for JGBs and Yen

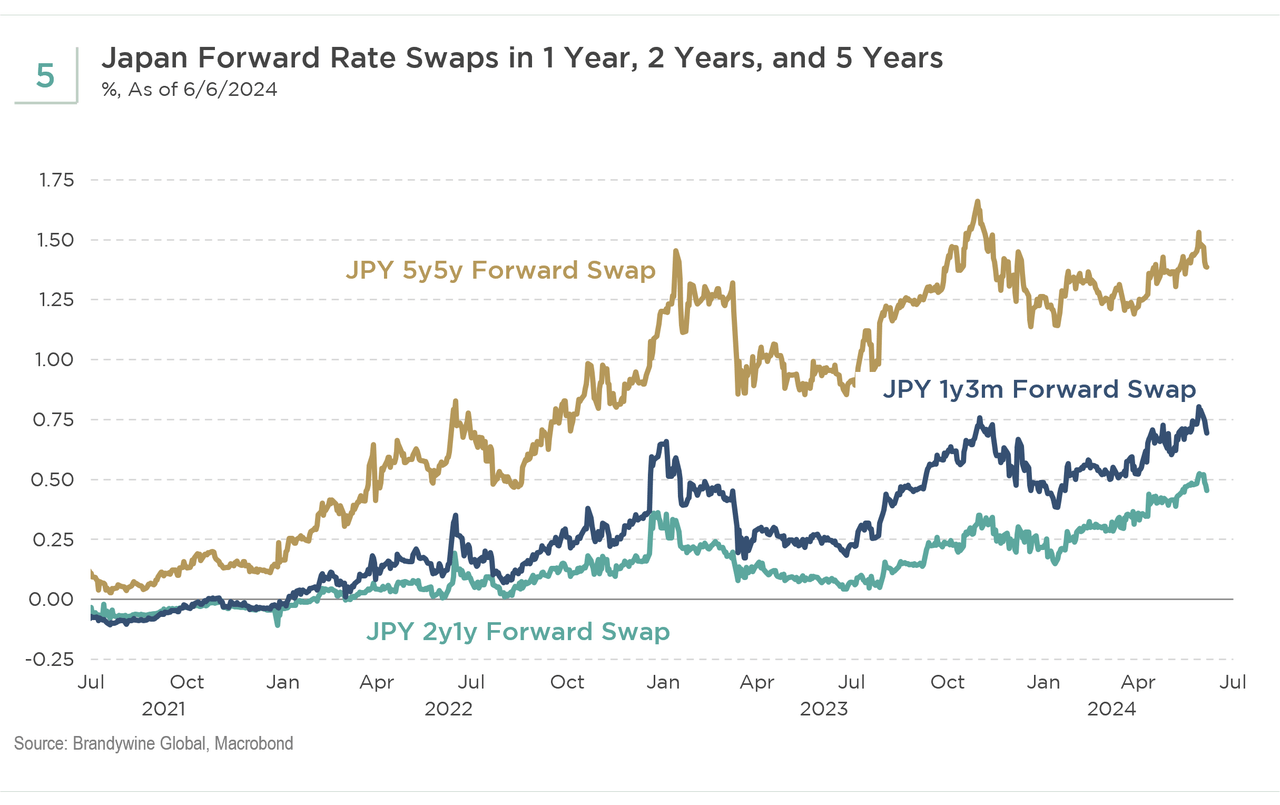

Recently, the yield on 10-year Japanese government bonds (JGBs) broke the 1% level, which has been a level targeted by yield curve control (YCC) previously. Therefore, a break above this now-removed ceiling is an important signal. The path of least resistance is likely higher rates from here. Currently, the swaps market is pricing in two rate hikes in the next 12 months and three rate hikes in two years (see Exhibit 5).

Given that we have yet to see a rebound in real consumption, the BOJ is still likely to move gradually, which the market currently is predicting. However, with Japan’s output gap – the difference between the economy’s actual and potential output – somewhat closed, an acceleration in real spending driven by wage growth could stoke inflation and put pressure on the BOJ to raise interest rates. In that event, it is very plausible that the market will scramble to price in multiple rate hikes over the next two years. And the yen, which has been the one of the most unloved currencies, will finally be able to rally as the interest rate gap with the U.S. narrows.

While that scenario seems somewhat further out in the universe, Japan could well be moving in that direction. And that would certainly play to Deputy Governor Uchida-san’s “this time is different” tune.

Index Definitions:

Consumer Price Index (CPI) is used to measure the change in the out-of-pocket expenditures of all urban households for a particular set of goods and services. In terms of its coverage, the CPI measures the cost of spending made directly by households for the items in its basket, with the notable exception that it also includes a measure of the rents that homeowners implicitly pay instead of renting their home.

Producer Price Index (PPI) measures the average change in selling prices over time received by domestic producers for their output.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here