Fund performance

Average annual total returns (%) for period ending June 30, 2024

|

Columbia Strategic Income Fund |

3-mon. |

1-year |

3-year |

5-year |

10-year |

|

Institutional Class (MUTF:LSIZX) |

0.82 |

7.26 |

-0.39 |

2.20 |

3.06 |

|

Class A without sales charge |

0.74 |

6.99 |

-0.64 |

1.95 |

2.79 |

|

Class A with 4.75% maximum sales charge |

-4.05 |

1.90 |

-2.24 |

0.96 |

2.29 |

|

Bloomberg U.S. Aggregate Bond Index |

0.07 |

2.63 |

-3.02 |

-0.23 |

1.35 |

|

ICE BofA U.S. High Yield Cash-Pay Constrained Index |

1.02 |

10.36 |

1.65 |

3.69 |

4.20 |

|

FTSE Non-USD World Government Bond Index |

-2.84 |

-2.19 |

-9.40 |

-5.02 |

-2.45 |

| JP Morgan Emerging Market Bond Index – Global |

0.44 |

8.35 |

-2.22 |

0.27 |

2.35 |

| Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiathreadneedleus.com for performance data current to the most recent month end. Institutional Class shares are sold at net asset value and have limitedeligibility. Columbia Management Investment Distributors, Inc. offers multiple share classes, not all necessarily available through all firms, and the share class ratings may vary. Contact us for details. |

- Columbia Strategic Income Fund Institutional Class shares returned 0.82% for the three months ending June 30, 2024, outperforming the benchmark.

- The fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, returned 0.07% for the same period.

- For monthly performance information, please check online at columbiathreadneedleus.com.

Market overview

Returns for the global bond market were mixed during the second quarter of 2024. The Federal Reserve’s preferred measure of inflation indicated persistent price pressures and clouded the outlook for future interest rate cuts. As a result, Treasury yields moved notably higher over much of April. That move lost momentum following the Fed’s meeting in early May after Fed Chair Powell downplayed the likelihood of restarting rate hikes, despite uneven progress toward taming inflation. Soon after, employment data registered a slower pace of job gains, suggesting that the pace of growth may have peaked. As the quarter progressed, the market largely settled on the view that while the timing and pace of Fed easing was uncertain, the central bank’s next move would be to lower the fed funds target. Treasury yields backed off year-to-date highs to finish the quarter modestly higher, with the 10-year bond (US10Y) closing at 4.39%. The broad U.S. Treasury market registered a slight gain of 0.10% for the period, as the income component outweighed the impact of rising yields on prices.

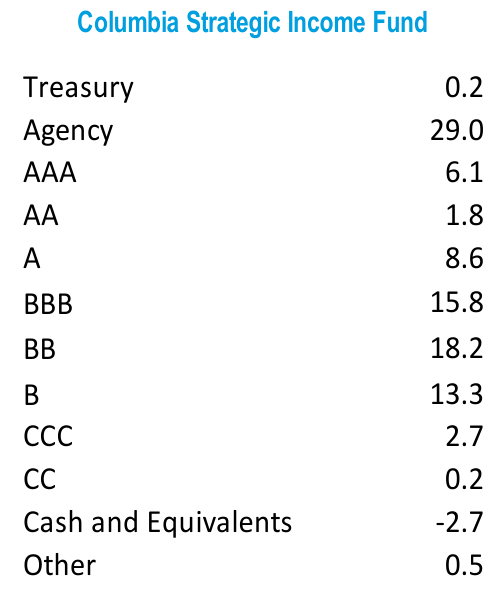

Credit Quality (%) as of June 30, 2024

|

Third-party rating agencies provide bond ratings ranging from AAA (highest) to D (lowest). When three ratings are available from Moody’s, S&P and Fitch, the middle rating is used. When two are available, the lower rating is used. If only one is available, that rating is used. If a security is Not Rated but has a rating by Kroll and/or DBRS, the same methodology is applied to those bonds that would otherwise be Not Rated. Bonds with no third-party rating are designated as Not Rated. Investments are primarily based on internal proprietary research and ratings assigned by our fixed income investment analysts. Therefore, securities designated as Not Rated do not necessarily indicate low credit quality, and for such securities the investment adviser evaluates the credit quality. Holdings of the portfolio other than bonds are categorized under Other. Credit ratings are subjective opinions of the credit rating agency and not statements of fact and may become stale or subject to change. Due to rounding, percentages may not add up to 100. |

While various growth metrics, including those related to the labor market, showed signs of cooling, the U.S. economy remained resilient during the quarter. While credit generally outperformed similar-duration U.S. Treasuries, that advantage narrowed in late June, as global election risk came into greater focus. Corporate credit spreads widened only modestly from historically tight levels, as investors capitalized on weakness to lock in elevated yields. Leveraged-loan prices rallied to their highest point in two years, aided by a record wave of repricings that triggered a persistent net-supply imbalance. As a result, the 1.87% total return of the Credit Suisse Leveraged Loan Index led fixed-income sectors during the quarter. Performance for investment-grade corporate bonds was marginally negative at -0.09% (Bloomberg U.S. Corporate Bond Index), while high yield generated a positive 1.09% total return (Bloomberg U.S. Corporate High Yield Index).

Top ten sector weights as of June 30, 2024

Portfolio attribution by risk factor

Institutional Class shares of Columbia Strategic Income Fund returned 0.82% during the quarter. Contributors and detractors from performance included:

- Duration: Interest rate risk contributed to absolute performance, as the income component of that exposure offset price declines as Treasury yields rose.

- Credit: Credit risk contributed favorably to performance, with the largest gains driven by residential mortgage-backed securities and high-yield corporates.

- Currency: Currency risk detracted very modestly from returns.

- Inflation: Inflation risk had no impact on performance during the quarter.

Outlook and positioning

For the first time in nearly two years, the risks to the economy have shifted. Instead of being uniformly upside risk, there is a growing balance in growth, the labor market and inflation. Real-time gauges of growth in the U.S. economy have downshifted from the 3%- 4% range to the 1.5%-2.5% range — not a recession, but also not a boom. Even though the labor market continues to generate more than 150,000 jobs per month, the unemployment rate has risen 0.7% from the lows. Lastly, inflation has settled into a continued descent toward 2% after a burst in the first quarter. This is not a prediction of a recession, but at least a more balanced outlook than 2023 provided.

Just like markets had not fully priced in the upside risks two years ago, especially in interest rate markets, it does not appear that markets have priced in this emerging downside. All maturities on the Treasury yield curve are yielding above 4%, and credit spreads are near long-term tights. If risks to economic growth and inflation are becoming more likely, this pricing does not seem sustainable. Again, this is a marked shift from the last two years.

Credit fundamentals, whether corporate or household, are still solid. Revenues and incomes are growing. There is no doubt deterioration on the margin — whether it is low- income households or over-leveraged companies — but this is not yet widespread.

However, valuations are unattractive because they fully reflect these positives and offer little cushion if the economic outlook erodes such that private-sector incomes or profitability are impacted.

In this environment of unattractive valuations and a more balanced set of risks in the future, we have positioned more conservatively in credit risk. Our tilt is not just toward higher quality credit such as mortgage-backed securities and asset-backed securities, but also toward shorter spread duration — and therefore lower volatility — bonds. We retain liquidity to capitalize on potential cheapening, while owning high-quality carry to maintain a competitive yield profile. In duration, we remain moderately longer than neutral in anticipation of a normalization of Treasury yields. With the skew of risks normalizing, we are focusing our duration exposure primarily on the sub-10-year area of the yield curve. This should also shield against volatility spurred by fiscal sustainability and Treasury supply concerns in the market.

Read the full article here