Freeport-McMoRan (NYSE:FCX) expects to report a disappointing quarter this week, but the key to the investment story is always the price of copper. Copper prices have slumped lately, and a pushback on EVs and renewable energy isn’t going to help in the short term. My investment thesis still remains Bullish on the stock after the recent pullback due to the strong cash flows produced at higher copper prices.

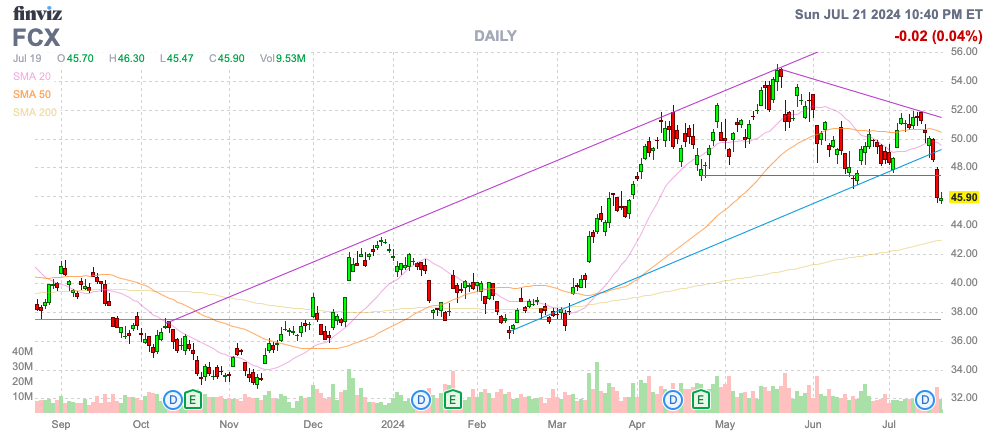

Source: Finviz

Tough Quarter

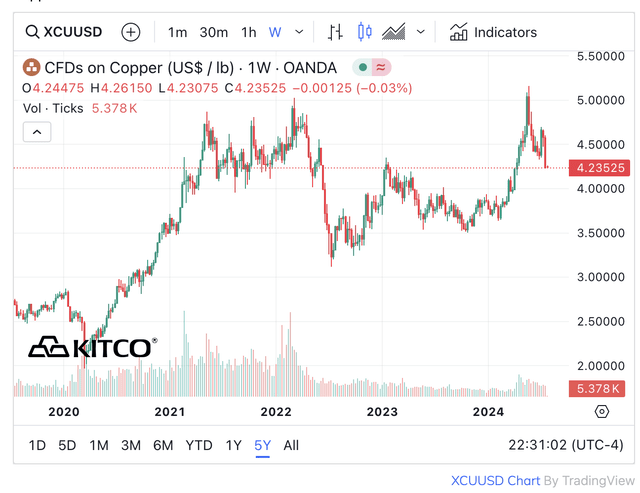

Along with Q1 results, Freeport-McMoRan guided to 2024 copper prices of $4.25/lb. Copper prices appeared headed to sustainable levels above $5/lb, but prices have suddenly slumped back to the target, and the company forecast a Q2 average price of $4.45/lb.

Source: Kitco

Even worse, the copper miner ran into copper export issues in Indonesia, leading to a disruption in shipping copper concentrates from PT-FI during June. Freeport-McMoRan recently guided to the following miss from the April 2024 targets:

- Copper is 5% below the 975 million pounds target.

- Gold 30% below 500 thousand ounces target.

Freeport-McMoRan obtained the export license on July 2 and expects to ultimately ship these copper and gold supplies later this year. In essence, the copper miner will report a weak June quarter, but future quarters will be boosted by the additional sales.

The current consensus estimates have the company reporting the following Q2 numbers on July 23 before the market opens:

- EPS of $0.38, up 8.3% YoY.

- Revenue of $6.0 billion, up 4.8% YoY.

If not for the higher copper prices, Freeport-McMoRan would’ve reported a much worse quarter, with copper volumes down substantially from the Q1 levels already. Regardless, the copper miner still guided to annual operating cash flows in the range from over $7.5 billion per year at $4/lb copper and over $11.0 billion per year at $5/lb copper.

Next Level Up

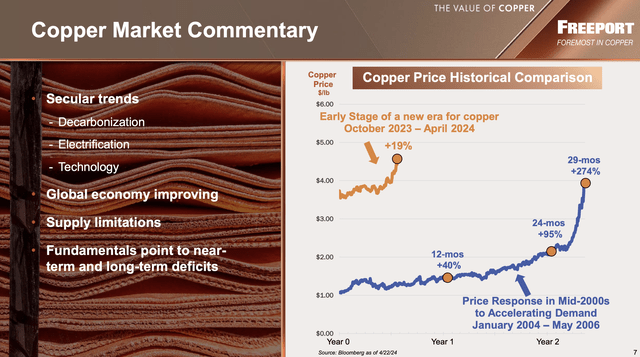

Freeport-McMoRan has made the case for copper prices to make a run similar to the mid-2000s. Copper went from $1/lb to $4/lb in just a couple of years, and the market could be in the midst of the next level higher.

Source: Freeport-McMoRan Q1’24 presentation

In this case, copper wouldn’t need to make a dramatic run with prices hitting record levels from $5/lb to $6/lb producing massive cash flows for Freeport-McMoRan. The company already highlighted how $5/lb leads to operating cash flows of $11 billion per year.

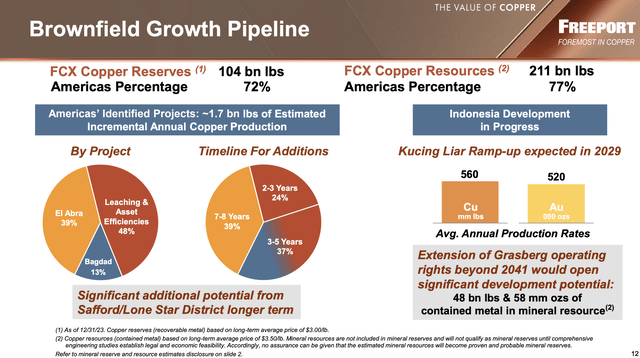

The other key to the copper miner is that the story isn’t necessarily built on current production. Freeport-McMoRan controls 104 billion pounds in copper reserves at a $3.00/lb price with 72% in the Americas and copper resources at 211 billion pounds at a $3.50/lb price with 77% in the Americas. The company has much more favorable taxes and ownership positions in the Americas, favoring the development of future production away from Indonesia.

Source: Freeport-McMoRan Q1’24 presentation

Freeport-McMoRan has the plans to add ~2 billion pounds of annual copper production by the 2030 timeline, or ~50% more than current production of 4 billion pounds annually. The copper miner has the assets to add more copper production in the more favorable Americas region, depending on the price of copper.

The key is that Freeport-McMoRan is spending $3.6 billion on capital expenditures this year and plans to increase this amount to $3.9 billion next year. The company has set aside an amount each year as discretionary allowing for immediate stoppage, if copper prices plunge, with the forecast at $1.3 billion in 2025.

The copper miner isn’t aggressively spending to build new copper production, despite the strong forecasts for future demand. The global push for EVs and renewable energy remains strong where copper use is 2x to 4x traditional vehicle and energy sources, but the risks definitely exist with former President Trump focused on eliminating EV subsidies.

The stock has a market cap of $66 billion and is a solid play on the cash flow picture with copper prices above $4/lb and, overwhelmingly, if copper prices were to surge beyond $5/lb for a sustainable period. With Sprott Energy projecting transport and grid demand for copper to overwhelm existing and future supply, Freeport could be right about much higher prices over the next few years.

Takeaway

The key investor takeaway is that Freeport-McMoRan is about to report a tough Q2, with copper and gold export volumes down. The investment story is never based on quarterly sales metrics. The ultimate key is the cash flow picture over the long term and the potential for higher copper prices for a company controlling vast amounts of copper reserves.

The recent weakness is another buying opportunity due to the long-term demand equation for copper, though the stock could be volatile as EV and renewable energy demand ebbs and flows from time to time.

Read the full article here