Wingstop Inc. (NASDAQ:WING) franchises and operates restaurants under the Wingstop brand, known for its offering based around wings. After Q1/2024, the company has a total system-wide restaurants of 2279, of which only 50 are company-owned and the rest franchised. The majority of restaurants are currently located in the United States, but the company also has a good number of international franchised locations.

The company is building an incredible growth story, as Wingstop continues to attract great sales, enticing franchisees to open up restaurants. In around nine years on the stock market, Wingstop’s stock has now returned 1759% as the company’s highly profitable growth has lured in investors.

Stock Chart From IPO (Seeking Alpha)

Setting the Scene: The Restaurant Industry Is Tough

The restaurant industry is incredibly competed in the United States as competing restaurant concepts fight for a share of the incredibly large market. Carving out valuable demand is overwhelmingly challenging for most restaurant chains – I’ve previously written about many up-and-coming publicly traded restaurant chains with an overwhelmingly negative tone, as achieving sustainable profitability is challenging even with notable scale. For example, I have written two articles with a Sell rating on GEN Restaurant Group (GENK), one article on Kura Sushi (KRUS), one article on Shake Shack (SHAK), and one article on Red Robin (RRGB).

More mature restaurant concepts still seem to have trouble sustaining growing, profitable operations, outlined by my articles on Cheesecake Factory (CAKE) and Dine Brands (DIN).

In the extremely challenging industry especially for growing concepts, Wingstop has managed to generate industry-leading margins with high, capital light growth, speaking for the concept’s massive success.

Wingstop is Building a Massive Success Story

Wingstop is building a massive success story in the challenging industry. The company’s success has been built on a franchising model, as only around 2% of the restaurants are company-owned. Wingstop continues to attract a great number of new franchisees and current franchisee expansions, as the company is outperforming the industry clearly in terms of same-store sales growth, pointed out in the Investor Day presentation. In Q1, same-store sales increased by an incredible 21.6% domestically, aided massively by the maturation of freshly opened stores.

The restaurant concept clearly resonates with customers as Wingstop continues to drive brand awareness and scaling the restaurant network. Wingstop’s impressive performance clearly paves a way for continued growth momentum into a globally recognized restaurant brand.

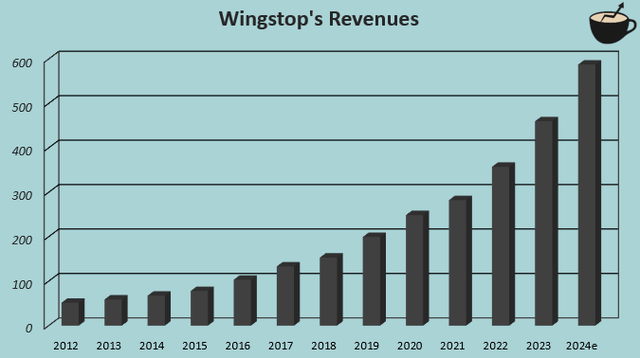

Author’s Calculation Using TIKR Data

Revenues have grown at a CAGR of 22.0% from 2012 to 2023, only accelerating as in Q1/2024 the growth stood at a highly impressive 34.1%. The current total restaurants of 2279 after Q1 are still a long way from Wingstop’s identified total opportunity – in the 2022 Investor Day, the company estimated long-term potential for 7000+ restaurants, of which 3000 are identified in international markets. If successfully scaled, the identified potential would more than triple the current sales, trailing at $497.1 million.

The company is following in the footsteps of Chipotle (CMG), which has been able to scale revenues into a current trailing $10.2 billion from low revenues in the early 2000’s – in 2004, Chipotle’s sales were $470.7 million, nearly the same as Wingstop’s currently. Chipotle works as an excellent example of a well-working restaurant concept’s ability to scale aggressively with great profitability.

The Ins and Outs of Franchising

Wingstop’s system-wide restaurants are built on franchised units – of the 2279 total restaurants after Q1, only 50 are operated by Wingstop as the rest are franchised units.

The franchising business model brings some clear advantages to Wingstop – the growth is incredibly capital light, as Wingstop has nearly non-existent net working capital and a relatively low $47.7 million in trailing capital expenditures. In addition, the company’s franchising revenues are very high margin as they are made through fees from franchisees with minimal costs related, making the current trailing operating margin 26.6%. With the margin profile, the earnings are low-risk as well in the short term as franchisees continue to pay relatively stable fees as long as a restaurant remains operative.

On the other hand, the franchising business model limits Wingstop’s financial potential – the comparison to Chipotle is in part misleading, as Chipotle operates all of its 3479 restaurants to generate the $10.2 billion in sales – with the franchising model, Wingstop’s earnings potential is much more limited than company-operated chains’ such as Chipotle. Dine Brands, predominantly franchising its, 3563 system-wide restaurants including the Applebee’s and IHOP chains, is able to generate current trailing revenues of $823.5 million.

To scale revenues near the level achieved by Chipotle and other large chains, Wingstop would need to acquire a significant amount of restaurants from its franchisees. In 2023, the company bought two locations, spending $10.8 million on the acquisitions. The company generated $95.8 million in sales from company-owned restaurants, and with an estimated average of 46 company-owned restaurants throughout 2023, the average sales of an owned unit comes up to $2.1 million.

With these estimates, an average unit costs around $5.4 million, bringing great revenues but lower margins as the $70.6 million in 2023 cost of sales brings the gross margin alone into 26.3% for company-owned restaurants, at around Wingstop’s entire operating margin even before company-owned restaurants -related operating expenses.

Another caveat to franchising is the lower control to the complete system-wide restaurants – Dine Brands has had issues in attracting new Applebee’s franchisees, and ultimately has little control over the restaurant concept’s total growth.

The franchising business model clearly brings many benefits, but limits Wingstop’s ability to scale revenues into the level that the often-compared Chipotle brings in. Unless an immense amount of capital is spent on acquiring franchised restaurants, the potential is capped at some point, even with the 7000+ total restaurants.

Valuation: Success Just Doesn’t Cut It Anymore

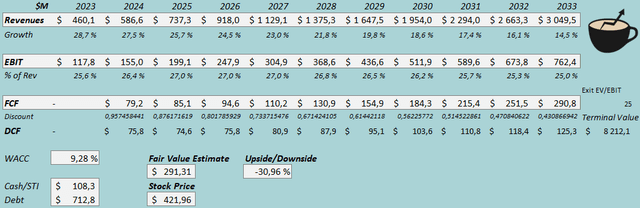

I constructed a discounted cash flow [DCF] model to estimate a rough fair value for the stock. In the model, I estimate Wingstop’s franchising success story to continue incredibly well, and for the company to start acquiring more franchised restaurants to scale revenues. I estimate acquired restaurants to scale gradually from an annual 5 in 2024 into 50 in 2033 at an average cost of $5.4 million per restaurant.

Due to the great franchising momentum and estimated acquired restaurants, I estimate revenues to compound at a CAGR of 20.8% in the decade from 2023 to 2033. For the EBIT margin, I estimate some benefit from scale into 27.0% in 2025, but for the margin to start slowly descaling into 25.0% as the company’s acquired revenues should generate much lower margins.

Excluding the restaurant acquisitions, I estimate a very good cash flow conversion considering the high growth. After 2033, I estimate an exit EV/EBIT multiple of 25, representing faith in continued growth after the year.

DCF Model (Author’s Calculation)

The estimates put Wingstop’s fair value estimate at $291.31, 31% below the stock price at the time of writing – Wingstop’s massive success story doesn’t cut it anymore at the current valuation. Painting an attractive scenario as an investment is increasingly hard, as my DCF model already accounts for great continued success.

CAPM

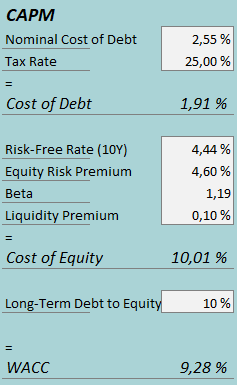

A weighted average cost of capital of 9.28% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Wingstop had $4.5 million in interest expenses, making the company’s interest rate an incredibly low 2.55% with the current amount of interest-bearing debt. I estimate a long-term debt-to-equity ratio of 10%.

To estimate the cost of equity, I use the 10-year bond yield of 4.44% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s estimate for the US, updated on the 5th of January. I use Aswath Damodaran’s estimated beta of 1.19 for the restaurant/dining sector. With a liquidity premium of 0.1%, the cost of equity stands at 10.01% and the WACC at 9.28%.

Takeaway

Wingstop is undeniably a massive success story in the challenging restaurant industry. The company continues to scale its system-wide franchise both domestically and internationally with an impressive revenue CAGR and high margins. While the franchising model brings in capital light, high-margin, low-risk revenues, the business model limits Wingstop’s earnings potential and partially limits the company’s control over the total system-wide restaurants, as Dine Brands has shown. Unless very rapid restaurant acquisitions from franchisees are made, the potential is capped even at the 7000+ total restaurants.

With my DCF model valuation, the company is priced for more than impressive success – while the great stock momentum seems to continue into eternity, the valuation already seems unsustainable. As such, I initiate Wingstop at Sell despite the company’s incredible continued success.

Read the full article here